In this edition of The Weekly, we share a condensed version of a new article by Abby Ross, CEO of The Resiliency Company, on the four convictions underpinning the opportunities in the Adaptation Economy.

Four convictions drive an evolving investment thesis in the adaptation economy:

1) The adaptation economy is large and growing; 2) Resilience makes for more durable investments; 3) Investors see predictable growth and opportunity in the adaptation economy; 4) It’s still early and underserved.

RSG 3-D's non-combustible panel system offers a financially competitive alternative to conventional construction that delivers wildfire, earthquake, and hurricane resilience.

Insights & ideas on resilience straight to your inbox. Were you forwarded this email? → Subscribe here

Bloomberg's investigation into America's "disaster industrial complex" finds that disaster spending now consumes nearly $1 trillion annually; that’s 3% of U.S. GDP, devoted to an endless cycle of preparing for and recovering from disasters. In the 1990s, the annual average was closer to $80 billion in current dollars.

“What that adds up to,” says Bloomberg reporter Eric Roston, “is a national economy that is spending more and more of its resources always recovering from disasters.”

Bloomberg’s "Prepare and Repair Index,” a list of 100 companies spanning waste haulers to engineering contractors to insurance companies, has outperformed the S&P 500 by 6.5% annually over the past decade.

Climate change guarantees that this will be a growth industry. The problem is that so much of this money can be spent more effectively: we continue rebuilding to outdated standards and maintaining insurance models that don't incentivize resilience. More resilient approaches to building, insuring, and investing exist. The challenge is implementing them.

As we've explored in our work on the Resiliency Delta, rebuilding to disaster-resilient standards costs more upfront—a 2025 Headwater Economics study found it adds $30,000 to rebuild a typical California home to wildfire-resistant standards. Yet insurance payouts typically fall short even of baseline reconstruction costs, let alone resilient upgrades. Homeowners must bridge that gap out of pocket.

The truth is we're already paying the resilience premium, just inefficiently. The disaster economy’s annual trillion becomes what Bloomberg describes as "a stealth tariff on consumer spending.” We're choosing to pay for cleanup and replacement—and ever-higher insurance premiums—on an endless loop, rather than paying once to build systems that withstand the storms.

The post-disaster window offers our best opportunity to break this cycle. When communities rebuild, homeowners are motivated, collective bargaining can drive down costs, and rebuilding can be more cost-effective than a retrofit. But working in this narrow window requires dedicated financing mechanisms that make resilient reconstruction accessible.

It's straightforward to invoice cleanup costs, but calculating the ROI of prevention is messier, especially when future disasters resist prediction. Still, a growing body of research confirms what common sense suggests: paying upfront beats paying repeatedly. The National Institute of Building Sciences found federal mitigation investments return $6 for every dollar spent; a study from Allstate and the U.S. Chamber of Commerce pegs it at $13-to-$1.

The disaster industrial complex isn't disappearing—but we can keep it in check. Here are three ways:

Financial products that make resilience accessible. At the homeowner level, we need new financing mechanisms that bridge the gap between insurance payouts and resilient reconstruction. Models like State Revolving Funds can allow states to finance infrastructure that safeguards property values and mitigates systemic risk.

Insurance innovations that reward resilience. The sector needs product innovation that incentivizes risk reduction, shifting from a purely reactive industry to one that drives resilient behavior.

Building standards that reflect tomorrow's climate reality. We have the technical knowledge; now we need to update codes and normalize using resilient materials, even if they cost more upfront. Projects like Dixon Trail, a ‘wildfire-resistant neighborhood,’ show what’s possible.

Those billions can keep chasing disasters, or we can redirect them to leverage points that save money in the long run. We're already committed to spending the money. What we get for it is still a choice.

Building Climate Resilience Through Insurance Incentives| Columbia Climate School | A Columbia Climate School project explores how insurance can play a proactive role—not just cover losses, but incentivize adaptation. The research finds that community-level mechanisms and local knowledge (e.g., farmers pooling insights) provide better risk identification than satellite data alone.

Protection or Profit? Transforming Home Insurance for Resilience | Climate & Community Institute | This policy brief from the Climate and Community Institute calls for a state-created “Housing Resilience Agencies”: public institutions that combine comprehensive risk reduction and decarbonization efforts and a public, single-payer disaster insurance program.

New York City Unveils Plan for Flood-Prone Neighborhood| Inside Climate News | After decades of chronic flooding, the low-lying Brooklyn–Queens neighborhood known as “The Hole” is finally getting a sewer system. The fix is a turning point for New York’s flood strategy: moving from patching up damage to building resilience.

Drought Is Quietly Pushing American Cities Toward a Fiscal Cliff| Grist | Drought is eroding the financial foundations of U.S. cities, from water utilities to property values. This piece reveals how long-term aridity threatens municipal budgets, and why local governments must treat water scarcity as a slow-motion economic crisis.

Read more about resilient public infrastructure and government solutions on The Epicenter here.

Real Estate & Construction

Building for the Storm Ahead: Climate Resilience in CRE | Commercial Property Executive | A real estate firm CEO talks about how his company integrates resilience into underwriting, design, and portfolio management. As storm risk escalates, developers are prioritizing resilient design, advanced materials, and tech-enabled monitoring.

Construction Costs for Wildfire-Resistant Homes | Headwater Economics| A new Headwater Economics study finds wildfire-resistant construction doesn’t have to cost a fortune. Researchers show that with simple material and design upgrades, homes can withstand growing wildfire threats with just a 2–3% increase in building costs.

Read more about resilient real estate on The Epicenter here.

Private Investment

Theresa Hoffmann on Reinventing Insulation for a Warming World | Climate Proof | In Climate Proof’s podcast, NANOPLUME CEO Theresa Hoffmann talks about a bio-aerogel insulation that’s thinner, lighter, and more heat-resistant. The biocompatible material could help buildings stay cool and efficient as heat waves intensify.

How Investing in Urban Resilience Can Foster Sustainable Growth | World Economic Forum | From New York to Cape Town, cities are finding that adaptation investments can do double duty, protecting residents while creating jobs. The private sector is responding: climate resilience technologies and services could attract more than $1 trillion in private capital by 2030.

From Recovery to Resilience: NYC’s Innovative Response to Hurricane Sandy | The Epicenter Editors | Our team recently interviewed Daniel Zarrilli, former Chief Resilience Officer for New York City and current Chief Climate & Sustainability Officer at Columbia University, about his work during the post-Hurricane Sandy recovery effort.

A Fiduciary Duty: Why the Housing Market Must Invest in Resilience | Alexis Pelosi | From stormwater systems to flood mitigation projects, we must redefine community-level investments in resilience not as a municipal cost, but rather as a direct investment in preserving property values and stabilizing the private cost of homeownership.

The Statistic of the Week

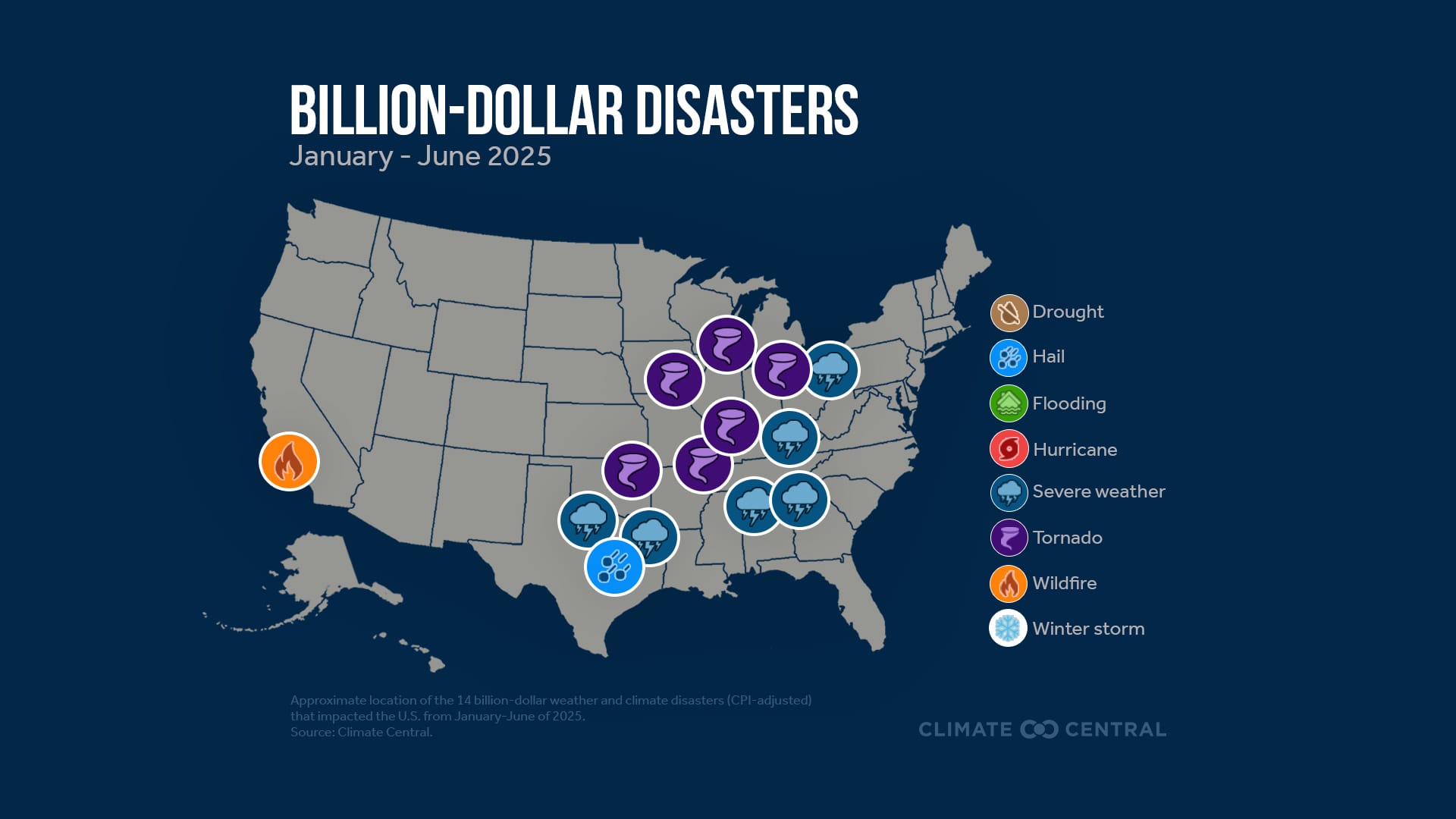

14 disasters

During the first six months of 2025, 14 billion-dollar disasters hit the U.S., costing $101.4 billion.

We had to share this stunning video of footage from inside the eye of Hurricane Melissa.

Have thoughts to share or want to add your voice to the conversation? Reach out!

The Epicenter helps decision makers understand climate risks and discover viable resilience solutions. The Epicenter is an affiliated publication of The Resiliency Company, a 501(c)3 nonprofit dedicated to inspiring and empowering humanity to adapt to the accelerating challenges of the next 100+ years.

The housing affordability crisis and the wildfire crisis aren't distinct challenges. They're a self-reinforcing cycle that requires investing in resilience to break.

The lack of standard home rebuilding playbooks, combined with the uneven delivery of federal disaster recovery funding, has led to fragmented rebuilding efforts over the past few decades. However, disaster recovery has evolved to more systematic approaches using pre-approved home plan catalogs.

Twenty-three billion-dollar disasters, $115 billion in damage, and not one hurricane: 2025 was a masterclass in how climate risk in the U.S. has changed.

Twenty-three billion-dollar weather and climate disasters struck the United States in 2025, revealing important takeaways for decision-makers in the real estate, public infrastructure, and insurance sectors.