The Weekly: How Data and Tools Enable Cities to Adopt Resilience at Scale

Cool roofs, permeable paving, green stormwater infrastructure, and strategic tree planting have all proven to reduce heat and flooding.

Cool roofs, permeable paving, green stormwater infrastructure, and strategic tree planting have all proven to reduce heat and flooding.

Several drivers are contributing to the rise in expensive severe convective storms: 1) population growth in high-risk areas; 2) non-resilient physical assets; and 3) rising building premiums.

Population growth in areas prone to severe storms has increased asset exposure and the physical assets in harm's way are not designed to withstand high winds or hail. Meanwhile, building premiums to rebuild after severe storms are increasing.

The California FAIR plan is proposing a huge rate hike, alongside incentives to reduce wildfire risk. The success of the effort hinges on cultivating a robust, affordable industry around fire-resilient construction.

Across the country, the geography of risk is redrawing itself. More and more homes find themselves marooned without private insurance—the ones with tides lapping at the front door, or encircled by blackened hills.

In the U.S., nearly three million properties now huddle under the fraying umbrella of state-backed “insurers of last resort.” California's FAIR Plan alone covers 645,987 policies as of September, a figure that has more than doubled in recent years as major carriers flee what they view as untenable risk.

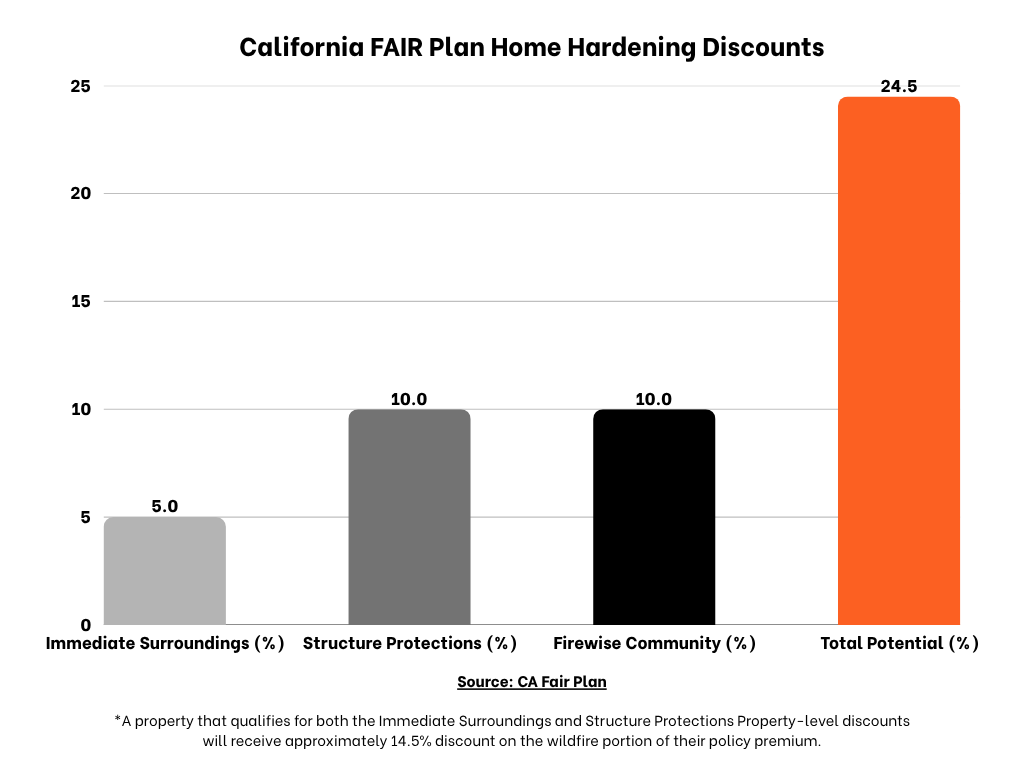

Last month, the FAIR Plan proposed a 35.8% rate increase, with changes potentially taking effect in less than six months in April 2026. Paired with this steep hike comes a glimmer of resilience: home hardening discounts offering up to 24.5% off wildfire premiums. Ten percent off for structural improvements. Five for defensible space. Another ten for membership in a Firewise community.

Can these incentives actually shift the calculus—and culture—of risk?

Home-hardening is “very akin to putting on a helmet before getting on a bike,” says Gabrielle Berthel, a forest advocate with the Natural Resources Defense Council. Yet, she says, “most of California’s fire budget goes to field treatments hundreds of miles away from communities, and so this is an extremely underfunded part of the wildfire mitigation conversation.”

For many homeowners, the hardening discounts could be serious money. The average annual FAIR Plan premium is around $2,800, but in the highest-risk zones, costs are vastly higher. In Santa Barbara, for example, insurance has become almost as elusive as rain; the average FAIR premium, as of March, was nearly $12,000. A full 24.5% discount on that figure would save $2,940 per year.

Yet even when fortifying a home is cheaper than rebuilding it from scratch, the expense can still exceed what most homeowners can reasonably afford. Headwaters Economics pegs the cost of core upgrades at $2,000 to $15,000. For full retrofits, the tab can hit six figures.

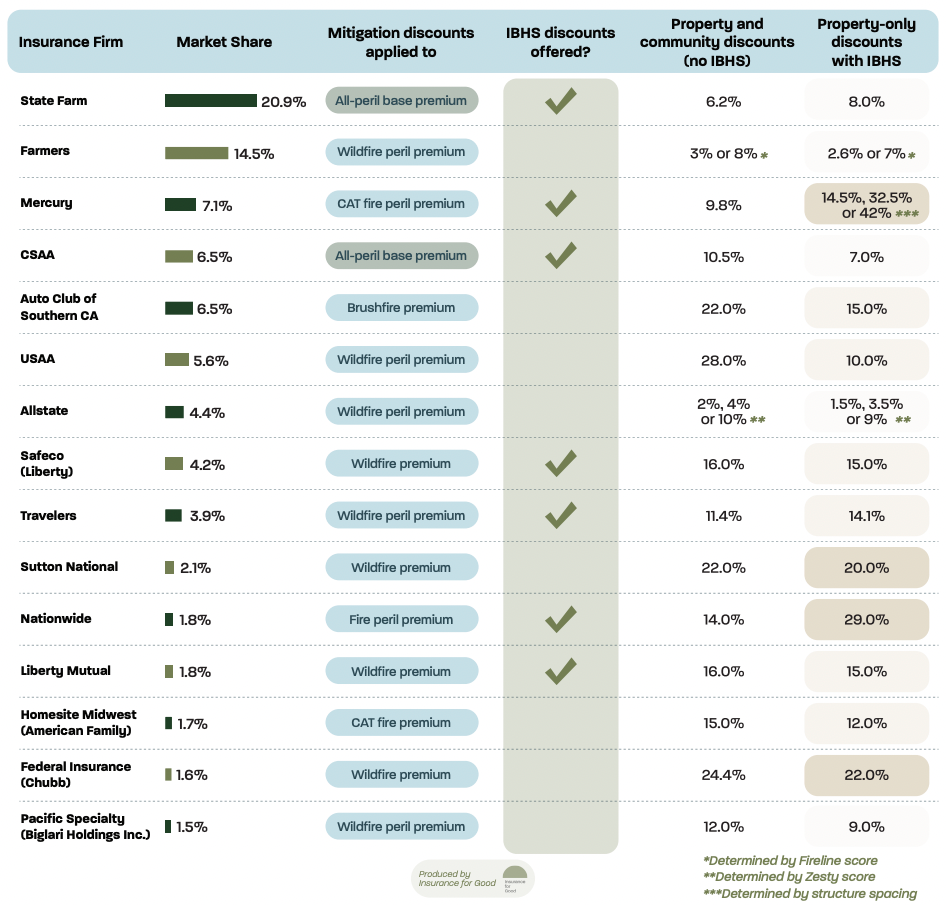

Private carriers in California have been required to recognize wildfire-risk reduction measures in their pricing since 2022, but incentives vary widely.

The FAIR plan’s maximum discounts are about 10% higher than the average maximum discount offered by private carriers—but they’re still not necessarily high enough to make expensive retrofits an obvious “yes.” Consider a 2,000-square-foot home in California that needs a Class A fire-rated roof to qualify for the 10% structural discount. According to the Headwaters Economics analysis, that could cost over $12,000. Even with the maximum possible FAIR discount, the payback period on that investment could stretch to ten years. That’s challenging math for homeowners already experiencing premium shock.

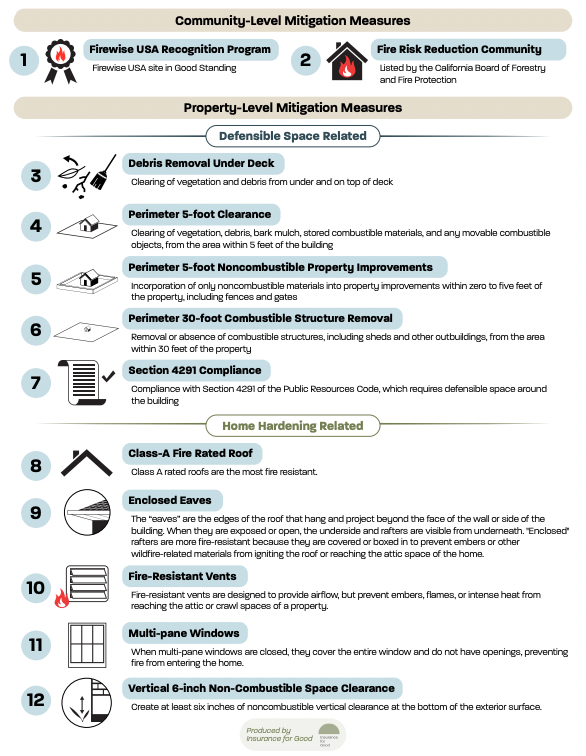

Fortunately, not all improvements require a massive construction loan. The home-hardening approach is a spectrum. “There's the defensible space stuff that you can do around your home, and that's often low labor, low cost. It's easier for folks to do themselves,” says Berthel. These are simple but powerful steps: clearing flammable vegetation within a few feet of the home, removing dead branches, and ensuring no wood fences or structures are right up against the house.

“It's the home improvement piece that can be a lot more expensive,” says Berthel. “That's also going to be on a spectrum. If you're working toward this certification, your house is getting better with every improvement you make.” An update to the discount structure, scheduled to go into effect on November 15th, will break improvements down into individual requirements, making it much easier to get incremental discounts for each upgrade.

Of course, then there's the other big question: who’s doing all these upgrades? Southern California’s construction sector was at 98% of peak staffing late last year. Across the state, labor costs are up 21% since 2019, and there are chronic shortages of skilled workers, which have been exacerbated by immigration sweeps.

Ultimately, a shift towards preemptive resilience depends on more than just discounts; it requires cultivating a robust industry of fire-resilient construction. “If we allow this industry to flourish and to get its feet under it, and to really become an industry where roofers and landscapers have this specialty, it'll be a huge economic boon to the state,” says Berthel. An Earth Economics analysis found that every dollar California invests in a home-hardening economy could return $1.70 in total economic activity.

In the beginning, as with many technology shifts, it will be easier for the wealthy to make these upgrades. Rob Moore, NRDC’s Director of Climate Adaptation, urges states to consider risk-reduction assistance for lower-income residents and affordable housing developers. “No one mechanism is sufficient to really get the market to change directions,” he says. Still, he believes premium discounts could help momentum start to build.

“There's a virtuous cycle to it,” says Moore. “Right as you begin implementing these programs, it creates capital flow. It creates benefits to the economy. You start building a workforce that is expert in doing these things, that allows these efforts to expand over time.” What begins as policy eventually becomes culture. “It’s something that builds upon itself.”

He’s seen this happen with hazards in other states. In Alabama, many years after the state started offering incentives to implement FORTIFIED roof standards, “you're at the point now where the majority of roofs getting installed in Alabama are not because of the incentives being offered,” he says. Rather, norms have changed—FORTIFIED roofs are now the default.

“That's a long way down the road for California's program. But you know, if you start seeing this becoming just the norm—where fire safe homes are the standard that people are building to? That's a very positive sign.”

It will take time to reach that tipping point. In the interim, homeowners will likely start with the smaller clearings and cleanings and purgings of combustibles. Each improvement winds the dial a few degrees closer to resilience.

“This is not a market problem that the insurance industry is going to solve for us,” says Moore. It isn’t an insurance crisis, he emphasizes; it’s an insurability crisis. “We have built a lot of things in a lot of places on a presumption that the risks would always stay the same, and climate change has turned that assumption on its head,” says Moore. Now, we have two options: help people move somewhere safer, or help them live in a way that reduces their vulnerability.

The real measure of progress isn’t smaller premiums, but homes that can stay standing in a world growing less predictable by the year. “If you just give people cheap insurance, their house will still burn down because you haven't really addressed the risk,” says Moore. “If you give people affordable insurance, plus help them reduce their risk—now you've actually given them safety and security.”

Have thoughts to share on this piece, or want to add your voice to the conversation? Reach out!

RSG 3-D's non-combustible panel system offers a financially competitive alternative to conventional construction that delivers wildfire, earthquake, and hurricane resilience.

The housing affordability crisis and the wildfire crisis aren't distinct challenges. They're a self-reinforcing cycle that requires investing in resilience to break.

The Epicenter’s three-part home catalogs series from Alexis M. Pelosi and Robin Keegan describes how we arrived at the current moment and explores what it means for the future of housing after disasters and in communities facing disinvestment, outdated zoning, or housing supply constraints.

The same principles that accelerate disaster recovery can address housing supply constraints, urban disinvestment, and affordability challenges in any market.