When benefits tied to investing in resilience can be measured and demonstrated, major new sources of capital become available to help finance resilience.

How public, private, and philanthropic leaders can scale the next chapter of climate resilience. A national call to action prepared for Chicago Climate Week and Aspen Ideas: Climate.

Bespoke deals are too complex to scale. Broad “green” designations are too vague to measure. A middle route can fund adaptation at the pace climate risk demands.

Hurricanes: Why They're So Destructive and Expensive

Hurricanes are the most costly type of climate disaster. The high cost comes from population growth in hurricane-prone areas, incentives that motivate rebuilding in those same areas, and physical assets in harm's way that aren't designed to withstand severe hurricanes.

PART 1: This is part one in a two-part briefing on hurricanes. Part two of this series focuses on the levers that exist to reduce these impacts.

Understanding Hurricane Costs

The 2024 hurricane season led to over $100 billion in economic losses and more than 320 deaths, with 17 named storms, including five major hurricanes. Before we break down the cost drivers making hurricanes so expensive, it’s helpful to understand the magnitude of their impact:

Hurricanes (and their direct consequences like flooding) are the most costly weather event.Hurricanes are historically the most costly climate event to impact the U.S., in terms of total dollars and average cost per event. The U.S. has had 400 billion-dollar weather disasters since 1980, costing $2.78 trillion in total, of which Hurricanes accounted for $1.3 trillion.

The biggest hurricanes occur less frequently, but produce the most damage. There’s an 80/20 rule for hurricane costs where Category 3, 4, and 5 storms comprise only 21% of all U.S. landfalling tropical cyclones, but account for 83% of all damage. The force multiplier of damage is wind speed.

The true costs of hurricanes are underreported and underestimated. The overall costs of disasters are underreported and don’t capture costs related to interrupted economic activity or loss of life. Hurricanes in particular have long-range impacts to human health with an estimated 15-year impact to total economic costs after each event.

Hurricane quick facts: - A hurricane is a low-pressure system that forms in the ocean with thunderstorm activity near the center of its closed, cyclonic winds. - A tropical cyclone becomes a hurricane when its winds exceed 74 mph. - Storms are categorized based on wind speed (Category 1 has wind speeds between 74-95 mph; Category 5 exceeds 157 mph). - Hurricane season is typically late May - Nov, with 97% of hurricanes happening in that window.

What about a hurricane causes the most damage?

Unlike wildfires or hail storms, the damages from hurricanes are multidimensional and stem from:

Storm surges: A storm surge is the rise of ocean water due to high winds as a hurricane reaches shore. It can rise 20-30 feet in height, fully submerging ground-level buildings along the coast. This 2-minute video captures a storm surge and tide in Ft. Myers Florida during Hurricane Ian.

Inland Flooding: Inland flooding, meanwhile, is caused by precipitation that exceeds the capacity of an area. In North Carolina earlier this year, rains from Hurricane Helene moved into mountainous regions where heavy precipitation flooded down through narrow valleys.

Tornadoes: Hurricanes can also cause the formation of tornadoes (a violently rotating column of air with winds that can reach 300 mph). Throughout Florida during Hurricane Milton, the National Weather Service issued a record number of 126 tornado warnings.

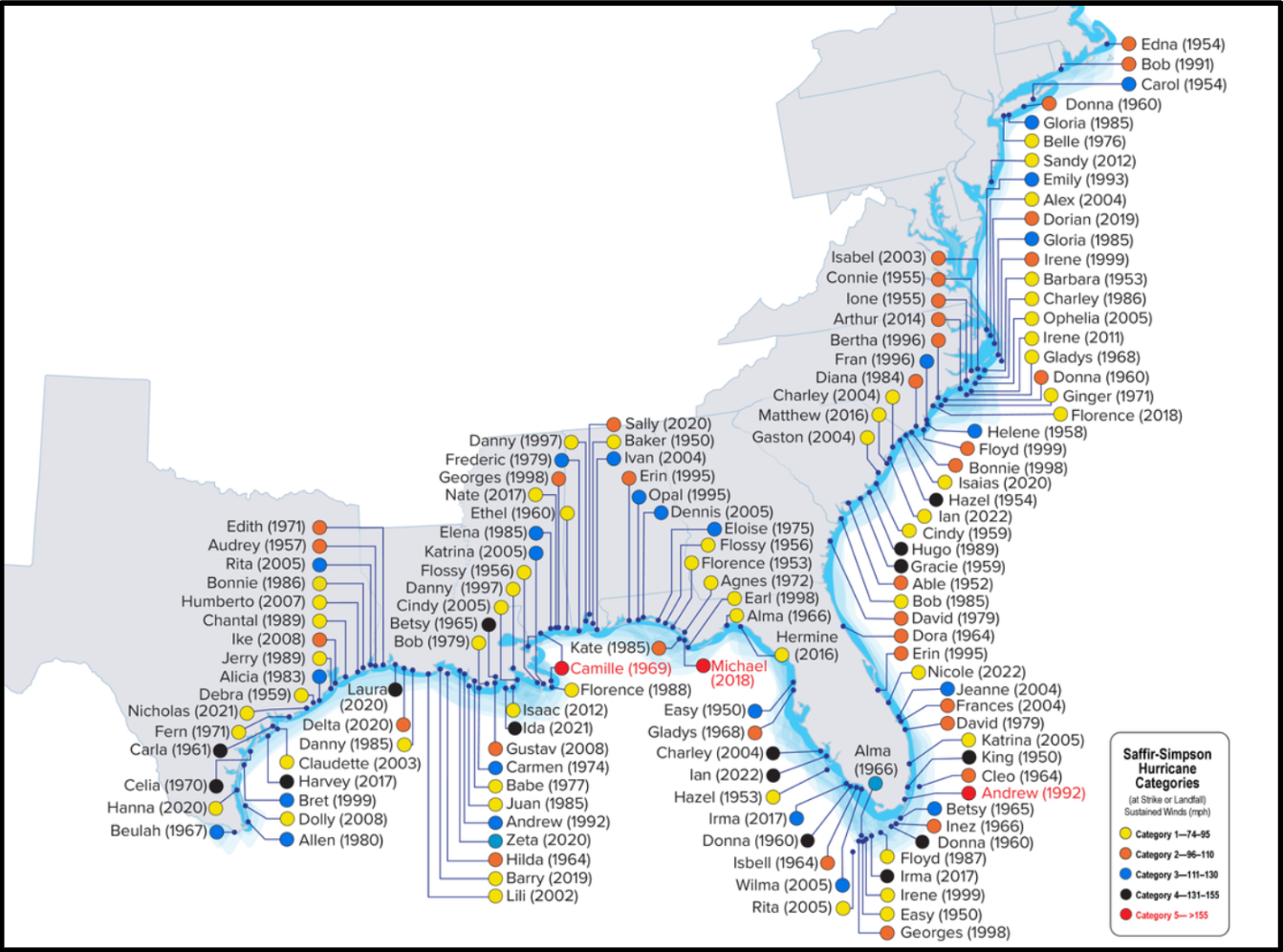

Of the 16 most expensive hurricanes (cost adjusted for inflation) in U.S. history, 15 have taken place since 2000 (the one outlier was Hurricane Andrew in 1992). What’s making recent hurricanes so costly? Here are four main drivers:

Population growth in hurricane-prone areas has increased asset exposure, leading to costly storms.

There are incentives to continually rebuild in the same hurricane-prone areas.

Assets that are more vulnerable to hurricanes translate into higher costs.

Storms are becoming more frequent and severe.

Driver #1: Population growth in hurricane-prone areas has increased asset exposure, leading to costly storms

More Americans today live in the paths of hurricanes. Americans are flocking to coastal areas; between 1970 to 2020, the population in coastal counties increased by 40 million people, or approximately 46%. For example, two coastal metropolitan areas–Houston, Texas and Tampa Bay, Florida–have grown significantly since 1980, with greater Houston adding 1.3 million homes. Even with updated construction to make buildings more resilient (as we’ll discuss in Driver #3), the savings from more resilient building codes and materials still can’t keep up with the increased costs from greater asset exposure. Swiss Re, a major global reinsurance company, suggests that all the hard-won gains from stricter building codes have been undermined by the explosion of growth along the coast.

As the population of coastal communities has grown, so has the value of physical assets in harm's way. Shoreline counties hold 50 million housing units, and $1.4 trillion of assets sit within an eighth of a mile of the coast. In Florida alone, home prices have increased 80% in just the last five years. Between 2013 and 2023, home prices in Florida grew 164%, making the state the second highest in single family home appreciation in the country.

Home prices in cities hit by hurricanes increased further after a hurricane hit. A 2021 study that compared home price appreciation in the year before and year after major hurricanes, found that in the year before Hurricane Katrina struck New Orleans, home prices were appreciating at 97% of the nationwide average. In the year after the storm, they increased to 109% of the nationwide average, on account of reduced supply but sustained demand. Similar results were observed from other major hurricanes across the southeast.

Research from 2023 corroborates this finding, but adds an important nuance: in the immediate period after a hurricane, incoming homeowners have higher incomes, leading to an overall shift toward wealthier groups and an evolution in the demographics (and inequality) of regions hit by hurricanes.

Rising housing prices push people to buy in flood zones. In the wake of Hurricane Sandy in New York, Joseph Tirone Jr., a broker with the real estate firm Compass, spoke to the relationship between the lack of affordable housing and asset risk: “The demand is insatiable. There’s really not much else people can buy, so they buy in flood zones.” This particularly impacts lower-income buyers, including immigrant families and many BIPOC households. Hurricanes also generally lead to less affordable rental housing while rent prices increase by 4-6% in the wake of a disaster.

Federal programs actually incentivize people to stay in high-hazard zones and not relocate. In the wake of a disaster, it’s common to hear, “We will rebuild.” The refrain speaks to America’s resiliency as a nation and the willingness of people who have lost everything to start again. The federal government provides a range of financial assistance following a disaster, including FEMA and the Small Business Administration’s Disaster Loan Program and a variety of pre- and post-disaster grants. Through its National Flood Insurance Program, FEMA also provides federally-subsidized flood insurance to supplement the home insurance of people living in flood-prone areas.

Driver #3: Assets that are more vulnerable to hurricanes translate into higher costs

Older homes are more susceptible to hurricane damage. Due to less resilient construction materials and building codes, older homes are more susceptible to heavier hurricane damage. For example, the average life span of a roof in Florida is 12-20 years, leaving homes built before 2002 more likely to break down from heat, moisture, and wind exposure.69% of the homes in the path of Hurricane Ian were constructed before 2000, meaning their construction was more vulnerable to wind speeds over 100 miles per hour (Hurricane Ian made landfall with 150 mph wind speed).

It’s worth noting that Florida’s current building codes, implemented in 2002, are considered to be some of the toughest in the country, and have resulted in reduced losses from hurricanes. The strengthened code requires more hurricane-resilient materials, construction and flood protection.

Driver #4: Storms are becoming more frequent and severe

Warmer waters and atmospheric temperatures fuel more intense storms. Warmer sea surface temperatures when combined with warmer atmospheric temperatures can create more intense storms with higher wind intensity. Extreme rainfall from Hurricane Harvey was 3x more likely due to a warmer atmosphere that can hold more moisture.

Sea level rise increases severity of flooding. Since 1900, sea levels have risen by 7-8 inches globally. While that might not seem like much, in low-lying regions the rise in sea level can dramatically increase the severity of flooding during a hurricane. A study of Hurricane Katrina estimated that higher sea levels led to more pervasive flooding throughout New Orleans. A study of Hurricane Sandy estimated that sea levels at the time increased the likelihood of flooding by 3x.

Conclusion

Between the increased frequency and severity of hurricanes and population growth into hurricane paths, there’s no question why hurricanes are so expensive. Add to that an aging housing stock and disincentives to relocate, and it might seem like hurricanes will continue to be as costly as they have been in recent years.

But as we explore in Part II of this Hurricanes briefing, there are specific opportunities to reduce that cost, reduce risk exposure, and fortify existing buildings and infrastructure in ways that mean less destruction and less cost.

Have thoughts to share on this piece, or want to add your voice to the conversation? Reach out!

Sign Up For The Epicenter

The Epicenter is a regular briefing that helps decision-makers understand the risks and impacts from climate hazards and discover practical, cost-effective resilience solutions.

By adopting green infrastructure in place of some gray infrastructure, Kansas City reduced the total costs of managing its combined sewer system through 2040 by over $2 billion.