RSG 3-D's non-combustible panel system offers a financially competitive alternative to conventional construction that delivers wildfire, earthquake, and hurricane resilience.

The federal government's retreat from climate adaptation has created a gap in data, funding, and coordination, but a new decentralized ecosystem of nonprofits, state governments, and coalitions is stepping up to fill the void and may prove more resilient to political disruption in the long run.

As federal disaster support shrinks, resilience districts offer local governments a promising new financing tool to fund climate adaptation on their own terms.

Insights & ideas on resilience straight to your inbox. Were you forwarded this email? → Subscribe here

Nowhere is the proverb “Necessity is the mother of invention" more true than in today’s insurance industry.

The frequency and severity of disasters are forcing insurers to rethink everything: from premiums to the products themselves. Insurers are racing to update their models, reduce exposure, and develop products for hazards that were once too diffuse or difficult to underwrite.

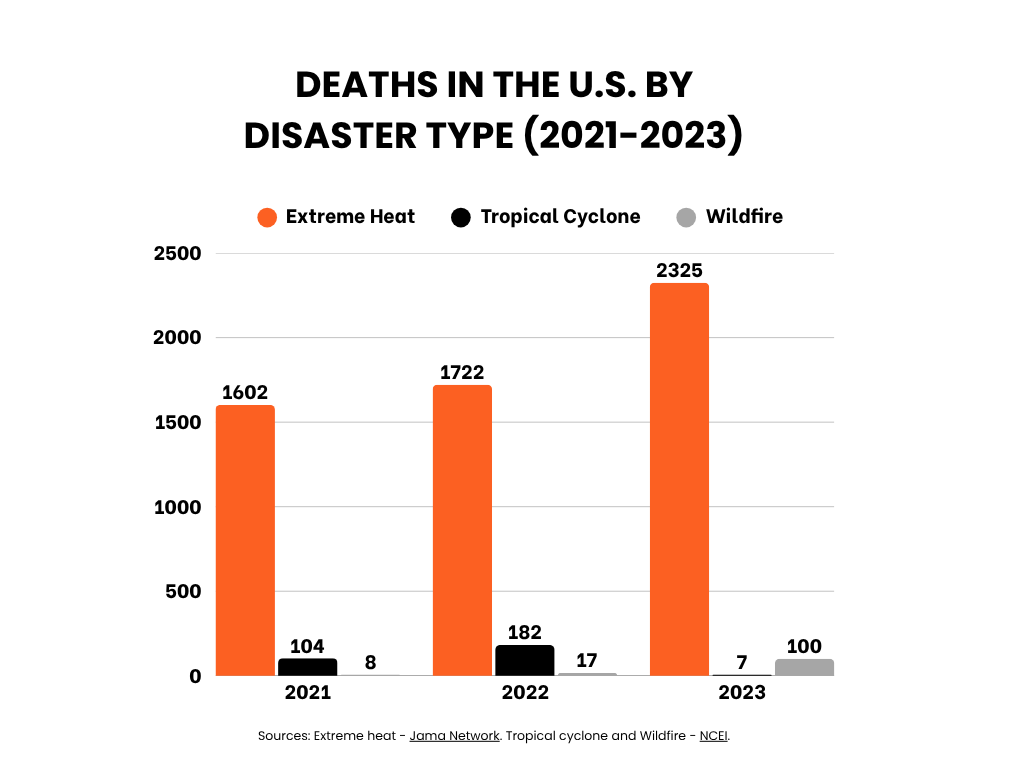

And the deadliest hazard in the United States is not wildfires or floods—it’s extreme heat, which killed over 2,000 people in the U.S. in 2023 alone.

Heat is a slippery risk to insure, as it often leaves no physical wreckage to tally. It erodes health, productivity, and infrastructure performance in slow, uneven ways; that makes it challenging for insurers that are built to cover tangible losses, not cascading human and economic strain.

The industry needs to create “entirely new approaches to making catastrophe risk more accessible,” said Roy Wright, CEO of the Insurance Institute for Business & Home Safety, in a recent conversation with The Epicenter about product innovation. Part of that is focusing on prevention rather than compensation. “Insurers must recognize the resilience actions their consumers and communities take,” says Wright. “This isn’t about discounts. It’s about understanding the risk and monetizing the reward for lower exposures.”

Enter: parametric heat insurance. These policies automatically pay out when a predefined extreme heat threshold is reached. They use an “if/then” trigger related to the event occurring; for example, “if the local temperature exceeds 100°F for 3 days, then pay $500 to the insured within days of the event happening.” In other words, parametric heat insurance is designed to allow outdoor workers to stay at home or take breaks on days when it may be unsafe to be outside—to help workers avoid exposure altogether.

Paying workers to stay home marks a shift in insurance thinking: incentivizing protective action rather than just compensating for harm. And it's a pattern that's increasingly showing up at the fringes of traditional insurance practices, like industrial and commercial mutual insurance company FM's $400 million in “resilience credits” for policyholders to protect themselves against threats like wind, flood, and wildfire. It's risk reduction as a business model, rather than an afterthought.

For now, the parametric heat insurance pilots remain small. The payouts are modest. But in places like Gujarat, India, where over 42,000 self-employed women now have access to parametric heat coverage that pays out when it’s unsafe to work, we're getting a glimpse of what's possible when the industry moves beyond traditional models. The question is how to scale it, tailor it to different regions, and get the right mix of partners involved to make it work.

Natural Disaster Claims in 2025 to Again Top $100B Despite ‘Abnormally Low’ Q3 Events | Insurance Journal|Even a “quiet” year isn’t enough to slow the mounting cost of climate disasters. Global insured losses are expected to top $100 billion for the sixth year in a row, raising questions about how much longer the insurance industry can absorb the blows.

New York Is Going to Flood. Here’s What the City Can Do to Survive. | The New York Times | This interactive feature maps out the rising tides, sinking land, and aging stormwater systems threatening NYC. Engineers and planners are considering a maze of upgrades, porous pavements, and giant sea walls to keep the next flood at bay.

From Ruins to Resilience: How 10 Cities Rebuilt Greener After Climate Disaster | One Earth | From Manila to New Orleans, cities hit hardest by floods, quakes, and hurricanes are rewriting the playbook for recovery. This story highlights ten places that turned catastrophe into a catalyst for greener, fairer, and more resilient infrastructure.

Read more about resilient public infrastructure and government solutions on The Epicenter here.

Real Estate & Construction

Turning Climate Resilience Into Real Estate Alpha | ClimateProof | Investor Hunter Maats argues that resilience is the next big differentiator in property markets. In this podcast episode, he talks about how climate-proofing assets is becoming a source of alpha for forward-thinking real estate investors.

Sustainability As Risk Mitigation in Real Estate Investing | U.S. Green Building Council | As climate risks rise, investors are re-evaluating what “safe” assets look like. This article breaks down how energy efficiency, low-carbon materials, and resilient design are becoming must-haves for protecting portfolios and property value.

Read more about resilient real estate on The Epicenter here.

Private Investment

Disaster Recovery Is Big Business | Bloomberg | Companies that prepare for, respond to, and rebuild after extreme weather are now outpacing the general market—making disaster response one of the country’s fastest-growing industries. This piece breaks down which sectors are booming, and why.

Can Planette’s AI Weather Help Forecast Climate Risk? | Sustainability Magazine | A new AI platform called Joro is designed to help insurers and financial firms anticipate climate risks. Planette thinks that more nuanced data will help these sectors maintain service quality as extreme weather escalates.

A Fiduciary Duty: Why the Housing Market Must Invest in Resilience | Alexis Pelosi | From stormwater systems to flood mitigation projects, we must redefine community-level investments in resilience not as a municipal cost, but rather as a direct investment in preserving property values and stabilizing the private cost of homeownership.

Resiliency Spotlight: Nanotech’s Cool Roof and Fire Mitigation Technology | The Epicenter Editors | If $1 invested in disaster prep saves $13, then it's clear investing in preparedness produces a higher ROI than recovery. But what does that preparation look like? An interview with Nanotech Materials offers an example of resiliency in the category of fortified roofing and building materials.

Investing to Minimize Flooding and Protect Critical Water Resources | Erin Delawalla | Historically, strong federal environmental regulations drove government action to manage water resources—that’s changing as more communities experience flooding and see the benefits of nature-based solutions to mitigate those impacts.

The Statistic of the Week

2.2%

The percentage of working hours worldwide that will be lost to high temperatures by 2030. That’s equivalent to 80 million full-time jobs.

Source: Aon and the International Labor Organization.

Have thoughts to share or want to add your voice to the conversation? Reach out!

The Epicenter helps decision makers understand climate risks and discover viable resilience solutions. The Epicenter is an affiliated publication of The Resiliency Company, a 501(c)3 nonprofit dedicated to inspiring and empowering humanity to adapt to the accelerating challenges of the next 100+ years.

The housing affordability crisis and the wildfire crisis aren't distinct challenges. They're a self-reinforcing cycle that requires investing in resilience to break.

Twenty-three billion-dollar disasters, $115 billion in damage, and not one hurricane: 2025 was a masterclass in how climate risk in the U.S. has changed.

Twenty-three billion-dollar weather and climate disasters struck the United States in 2025, revealing important takeaways for decision-makers in the real estate, public infrastructure, and insurance sectors.

Property insurance markets across the U.S. are under strain as premiums rise and insurers pull back from high-risk regions. In response, a growing number of states are leaning on public and quasi-public reinsurance backstops.