RSG 3-D's non-combustible panel system offers a financially competitive alternative to conventional construction that delivers wildfire, earthquake, and hurricane resilience.

The federal government's retreat from climate adaptation has created a gap in data, funding, and coordination, but a new decentralized ecosystem of nonprofits, state governments, and coalitions is stepping up to fill the void and may prove more resilient to political disruption in the long run.

As federal disaster support shrinks, resilience districts offer local governments a promising new financing tool to fund climate adaptation on their own terms.

Insights & ideas on resilience straight to your inbox. Were you forwarded this email? → Subscribe here

Who pays for resilience? And how does it get financed?

Every conversation at Climate Week in New York seemed to return to these questions.

On Monday, The Resiliency Company co-hosted the Adaptation Forum, a gathering that convened over 200 private investors, insurance company representatives, community leaders, and government officials to explore bright spots and innovations in adaptation and resilience.

Speakers at the Adaptation Forum highlighted that effective adaptation and resilience solutions are all around us. But with disasters occurring more frequently, with more severity, and in more places across the United States, we need to scale these solutions and models, and scaling requires new financial products and innovations.

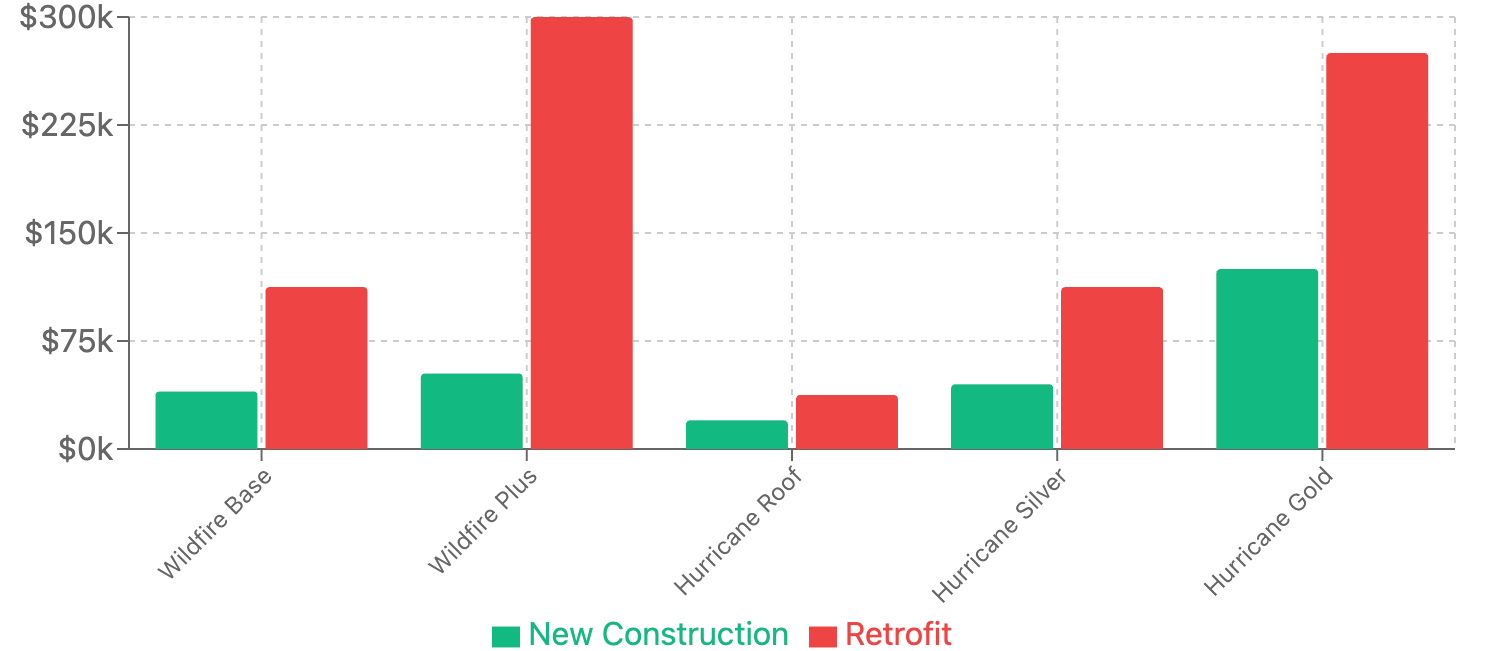

Consider home fortifications. A 2025 report from Headwater Economics found that rebuilding a 2,000 square-foot home in California to meet the state’s wildfire-resistant standards adds $30,000 to construction costs—up to a 10% premium on typical construction costs. When most insurance payouts fall below the baseline replacement costs of construction, many homeowners are left to cover these improvements out of pocket.

The stakes are high. Homeowners in areas prone to repeat disasters could lose their insurance entirely—a phenomenon currently occurring in California, as insurers decide to cancel policies and leave the state. Since 2019, one in five homes in the most extreme fire-risk areas of California have lost insurance coverage.

But after a disaster, such as the Los Angeles fires in January, there’s an opportunity to rebuild with resilience in ways that are less expensive than home retrofits. This is because it can be less costly to rebuild from the ground up to new standards than to retrofit existing structures, one by one. To rebuild an entire home to meet the IBHS standard of a Wildfire Prepared Home, it can cost between $35,000 and $60,000 more than it would cost to rebuild to current building codes. To retrofit an existing structure, costs often start at $150,000.

This is the "Resiliency Delta" – the difference in what financing options currently cover and what it takes to build to the highest safety and damage prevention standards.

While government, insurers, and mortgage holders all benefit from a resilient housing stock, homeowners ultimately bear the long-term risk of losing their homes or having them become uninsurable. We need financial products that address this specific problem.

The good news is that there’s plenty of precedent for designing financial products for homeowners. The Federal Housing Administration (FHA) offers a blueprint for what’s possible. Founded in 1934, the organization was created to make homeownership more affordable at a time when only one in ten Americans owned a home. The FHA reduced down payment requirements, extended loan terms up to 30 years (most loans in the 1920s and 1930s spanned 3-5 years), and introduced the concept of FHA loans for first-time homebuyers.

We need that same innovative spirit today—but focused on financial products that make climate-resilient retrofits and rebuilds affordable for every homeowner.

Read the rest of the article by Resiliency Company CEO Abby Ross here.

Financing the Resiliency Delta | Abby Ross | Rebuilding or retrofitting a home to a disaster-resilient standard means paying a premium—up to a 10% premium on typical construction costs. That burden often falls on homeowners, which is why we need new financial products.

Rethinking Risk: Why Local Governments Can’t Shoulder Climate Burdens Alone | Matt Posner | Approximately 80% of U.S. infrastructure is funded, built, and maintained by city councils, county boards, and state legislatures. Should local governments be expected to foot the entire bill for resilience as aging infrastructure, escalating climate risk, and other factors converge to leave local communities less prepared to absorb their growing risk? This article explores alternatives, including an emerging blueprint.

From Disaster to Blueprint: How Greenline's Model Could Transform Post-Fire Recovery | The Epicenter Editors | The Greenline Housing Foundation is helping Altadena residents recover, rebuild, and remain in the neighborhood following January's devastating fire. This profile of Greenline’s work examines how rebuilding with resiliency can drive a recovery that preserves wealth and helps residents return home.

Public Infrastructure: Rethinking our assumptions and financing tools for community resilience | Brookings Institution | Co-authored by Matt Posner of The Resiliency Company, this research brief from Brookings argues that our system of public finance, still dominated by the “tax-and-bond” model at the local level, is essential but insufficient to finance resilience measures. To pay for resilience—including infrastructure that reduces loss, protects insurability of property, and preserves affordability—we need a new wave of locally focused financial innovation to match the scale and urgency of the challenge.

Read more about resilient public infrastructure and government solutions on The Epicenter here.

Insurance: To address rapidly rising property insurance premiums, a new startup wants to turn property insurance volatility into a predictable bet | Moving Day | Rising and volatile property insurance premiums represent one of the few ways to get homeowners and policymakers to pay attention to escalating climate risks. This piece profiles Eventual, a startup that sees an opportunity to sell a hedge against that volatility. Their product, called Premium Lock, works like a parametric policy—paying out if a buyer's insurance premium increases more than a predetermined percentage or amount.

Read more about insurability on The Epicenter here.

Real Estate: Real estate speculators are swooping in to buy disaster-hit homes | WIRED | After the Eaton Fire in Altadena, California, in January, half of home purchases were by limited liability corporations—a statistic that speaks to “disaster gentrification,” the process where speculative investors will buy affected homes or lots. “Disaster investors” recognize that the value of the land can bounce back after a disaster, allowing them to make a quick profit, as long as they move fast and capitalize on the crisis.

Read more about resilient real estate on The Epicenter here.

Read more about resilient public infrastructure and government solutions on The Epicenter here.

Have thoughts to share or want to add your voice to the conversation? Reach out!

The Epicenter helps decision makers understand climate risks and discover viable resilience solutions. The Epicenter is an affiliated publication of The Resiliency Company, a 501(c)3 nonprofit dedicated to inspiring and empowering humanity to adapt to the accelerating challenges of the next 100+ years.

The federal government's retreat from climate adaptation has created a gap in data, funding, and coordination, but a new decentralized ecosystem of nonprofits, state governments, and coalitions is stepping up to fill the void and may prove more resilient to political disruption in the long run.

As federal disaster support shrinks, resilience districts offer local governments a promising new financing tool to fund climate adaptation on their own terms.

Resilience districts give local governments a new financing mechanism to fund climate adaptation, but their success depends on applying a forward-looking, risk-informed approach rather than defaulting to traditional bond financing logic.

The housing affordability crisis and the wildfire crisis aren't distinct challenges. They're a self-reinforcing cycle that requires investing in resilience to break.