Downpours are getting heavier across most of the U.S., and aging drainage systems are struggling to keep up. In response, a fast-growing municipal policy solution is scaling across the country.

We need to move beyond asking simply, How do we fund this project? and start asking, What financial risk does this community face, what outcomes could change that trajectory, and how should we invest accordingly?

Severe Storms: The Cost Drivers Making Them So Expensive

Population growth in areas prone to severe storms has increased asset exposure and the physical assets in harm's way are not designed to withstand high winds or hail. Meanwhile, building premiums to rebuild after severe storms are increasing.

PART 1: This is Part I in a two-part briefing on severe storms. Here we deconstruct the drivers making severe storms so costly. Originally published in January 2025, this briefing was updated in March 2026 to reflect more current numbers.

In Part II, we outline the levers that present opportunities to reduce the impacts and costs of severe storms.

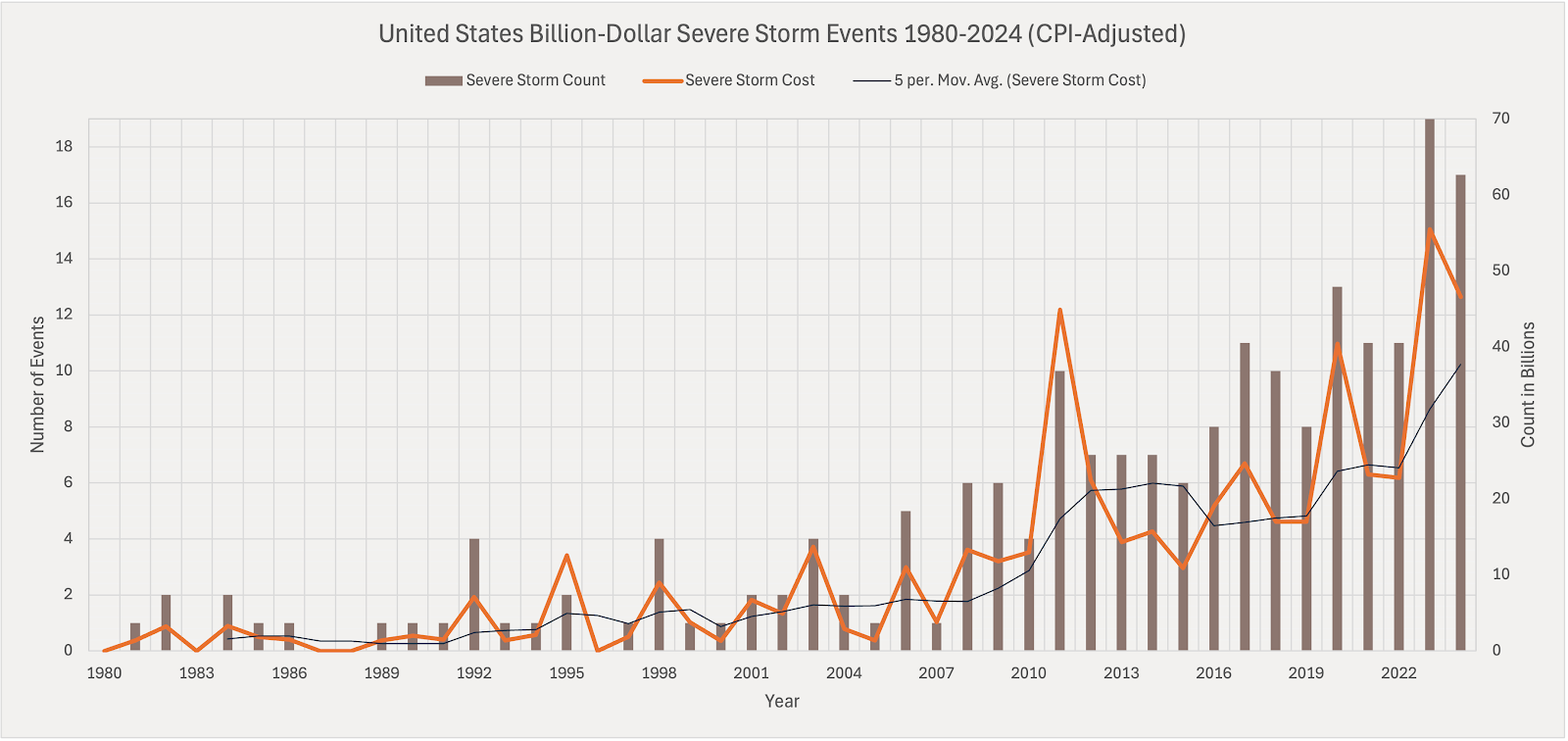

Severe storms are the most frequent billion-dollar disaster type in the U.S. Since 1980, one in every two disasters that exceeded $1 billion in damage has been a severe convective storm, defined as a storm with high wind gusts exceeding 58 miles per hour, a tornado, or hail.

In 2025, this trend accelerated. Of the 23 disasters that crossed the billion-dollar threshold in the U.S. last year, 21 of them (91%) were severe storms, causing roughly $51 billion in damages.

But severe storms weren’t always so common. According to NOAA, the frequency of billion-dollar severe storms began climbing around 2006. Since then, it’s shot up.

What’s going on? Are bigger storms hitting in ways they didn’t used to? Or are the same storms just more expensive now? In this briefing, we’ll outline the drivers contributing to a rise in expensive severe storms and the possible levers to reduce their cost in the future.

The Growing Costs of Severe Storms

Severe storms are classified by the insurance industry as secondary perils, natural disasters that are more frequent but less destructive and costly. In contrast, primary perils like hurricanes and earthquakes are less frequent and more destructive.

As an example of a primary peril, Hurricane Helene’s total costs exceeded $78 billion. It’s rare for a severe storm to cause damage that costs so much, but recent trends around their frequency and costs are staggering:

The average per-event cost of a severe convective storm is now 31% higher than it was in the previous decade.

Between 2022 and 2023 alone, there was a 90% increase year-over-year in economic losses due to severe storms.

In 2023, the entire U.S. insurance industry reported $60 billion in losses from severe storms. A 2025 survey found that insurance executives viewed severe storms as the leading threat to their balance sheets.

In 2025, of the $170 billion total insured losses from all natural catastrophes globally, severe storms comprised $61 billion (or 48% of that total), and most of those severe storms were in the U.S. That’s the third‑highest severe storm total on record.

What is a severe storm?

The term “severe storm” is a bit of a catch-all spanning storms that 1) have high-speed winds and/or tornadoes, or 2) have hail. Flooding often accompanies such storms, but NOAA considers flooding a separate disaster type. In this briefing, we explore two types of damage from severe storms:

Damage from tornadoes, derechos, and other high-wind storms

Damage from hailstorms

Note: Severe storms typically occur in warmer climates and during warmer seasons. They’re different from winter storms—also increasingly billion-dollar disasters—which occur in colder climates, during colder seasons, and include costs associated with snowfall, freezing rain, strong winds, icy roads, and freezes.

Damage from tornadoes, derechos, and other high-wind storms

The number of tornadoes in the U.S. has grown only slightly over the last three decades, so variability in damage from year to year has more to do with where a tornado happens to touch down. Since 1980, the annual number of hurricanes has remained steady at an average of around 1,200 tornadoes per year. In 2022, over half of all the tornadoes recorded caused no property damage, and 95% of them caused no injuries or fatalities.

The 1,341 tornadoes in 2022 cost a combined total of $700 million, and nearly all of that cost came from just one tornado in Nebraska in June of 2022. The costs from tornadoes vary wildly from year to year, based on where they touch down and what’s in their way. According to an analysis of NOAA data, tornadoes caused $43.6 billion in damage in 2023 alone—a major jump from 2022 and the highest in the last decade.

2024 and 2025 were both particularly active tornado years. With 1,735 confirmed tornadoes, 2024 had the second-highest count on record. In 2025, there were 1,559 tornadoes, the fifth-largest annual tornado count on record. The 2nd most costly disaster of 2025 (after the L.A. fires) was March’s tornado outbreak across central, southeastern, and eastern states, which caused $11 billion in damages.

Tornadoes are not the only high-wind events that can cause damage. Derechos, or widespread windstorms (compared to more centrifugal tornadoes), have also been major sources of damage.

Damage from hailstorms

Damage from hail is clobbering the insurance industry. Hail is a major driver of the costs incurred from severe storms. In 2024, the insurance company State Farm alone paid out over $5 billion in hail claims.

While the average frequency of hailstorms isn’t increasing, the costs from hail-related damages are. Since 2022, the number of insurance claims resulting from hail events has increased by more than 40%.

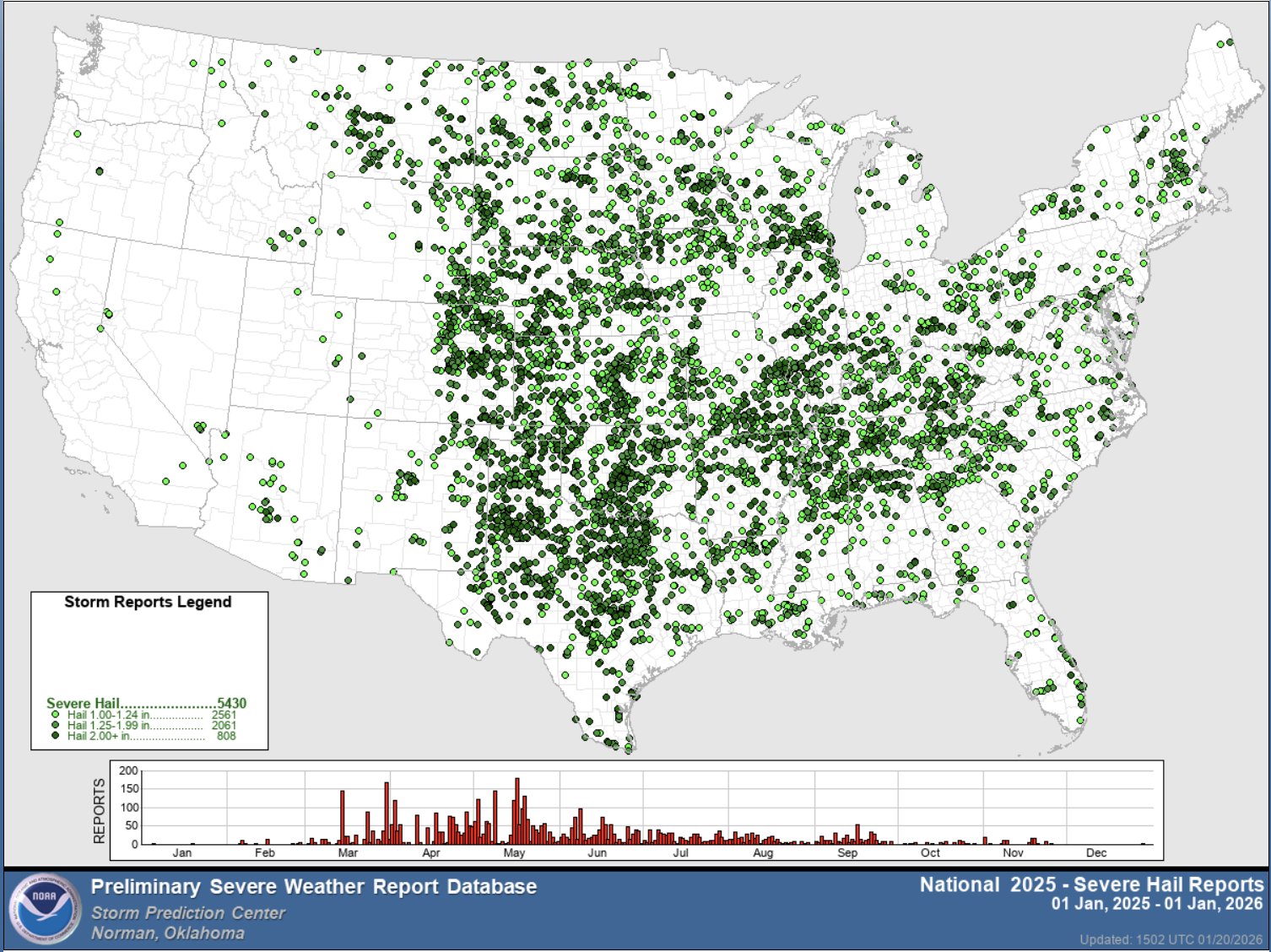

This map from the National Weather Service Storm Prediction Center outlines the geographic location of hailstorms for 2025.

Damage from flooding and lightning strikes

In addition to high winds, tornadoes, and hail, severe convective storms often produce heavy rainfall, flooding, and lightning strikes. In the U.S. each year, insurance companies pay approximately $1 billion in lightning-related claims.

Damage caused by the heavy rain and flash-flooding from severe storms leads to costly recovery, but NOAA considers flooding to be a separate (though related) disaster type. For the purposes of this briefing, we won’t focus on damages caused by flash-flooding from heavy rain (stay tuned for a future briefing on non-hurricane-related flooding).

The Cost Drivers of Severe Storms

Three main drivers are contributing to the rapidly growing costs associated with severe storms:

Population growth in areas prone to severe storms has increased asset exposure.

The physical assets in harm's way are not designed to withstand high winds or hail.

Building premiums to rebuild after severe storms are increasing.

Driver #1: Population growth in areas prone to severe storms has increased asset exposure.

Population growth in areas prone to severe storms has positioned more assets in harm’s way. Today, more people in the U.S. live in areas prone to severe storms as population growth transforms former farmland into suburbs.

For example, between 2022 and 2023, Texas—a state prone to severe storms—was the fastest-growing state in the nation and has grown by 40% in the last 20 years. In the first half of 2023, Texas accounted for the majority of nationwide hail-related losses, from roof damage on residential homes to hail-damaged cars on dealership parking lots. Meanwhile, the South—a region also prone to hail and storms—accounted for 87% of the U.S.’s 2023 growth, and added 1.2 million more people in 2025. Texas continues to lead the nation in population growth.

The reinsurance broker Gallagher Re found that between 2010 and 2020, Dallas-Fort Worth, Austin, and Denver—population centers in areas prone to severe storms—grew their housing stock by 12%. The concentration of new housing stock in metropolitan and suburban areas increased the impact and damage resulting from severe storms. “What may have been a remote severe convective storm event located just outside a suburb 10 or 20 years ago, now would have a greater likelihood of impacting a larger swath of exposures leading to significant insured loss,” the report said.

Driver #2: The physical assets in harm's way are not designed to withstand high winds or hail.

Many physical assets are vulnerable to damage from severe storms. Roofs are old and not built with impact-resistant materials. Garage doors aren’t wind-rated. HVAC units are missing protective screens. Windows aren’t storm-proof.

In 2022, State Farm reported that 80% of total hail claims paid come from homeowners, and the vast majority of homeowner-related claims were for repairing and replacing roofs. Roofs in hail-prone areas last, on average, half as long as roofs in areas that don’t experience hail (10 years vs. 20 years) because they need to be replaced more frequently. This also doubles the cost to insurance companies over the same period of time. With the average roof costing approximately $10,000, insurance companies are paying an average of 2x that cost over 20 years.

But there is a new physical asset that is costly and exposed: solar panels. A brief hailstorm in 2019 destroyed more than half of Texas’s Midway Solar power plant’s 685,000 photovoltaic panels, causing $70 million in damage. In 2024, hail damaged thousands of panels at a solar farm in Fort Bend County, Texas.

Driver #3: Building premiums to rebuild after severe storms are increasing.

The cost to rebuild is also making storms more expensive. According to Swiss Re, building costs are rising faster than the overall rate of inflation, which leads to higher reconstruction costs and higher claims. Meanwhile, the average claim amount is increasing as the value of assets increases. Many roofs have solar panels on them, and such panels are insured but still vulnerable to severe storms. When hit by hail or high winds, the claims are now higher. Today, 7% of all homes in America have solar panels, but that number is projected to double by 2030.

Conclusion

Similar to the findings in our hurricanes analysis and briefing, there is no panacea that can dramatically reduce the costs of severe storms. More people and more assets in more places that are likely to experience severe storms translate into higher costs. But there are steps that the private sector can take to fortify the assets across America’s heartland where such storms are most common. We are far from sitting ducks; resilient approaches and materials can be the difference between total destruction and light damage. In that delta, millions of dollars can be saved.

Have thoughts to share on this piece, or want to add your voice to the conversation? Reach out!

Sign Up For The Epicenter

The Epicenter is a regular briefing that helps decision-makers understand the risks and impacts from climate hazards and discover practical, cost-effective resilience solutions.

Downpours are getting heavier across most of the U.S., and aging drainage systems are struggling to keep up. In response, a fast-growing municipal policy solution is scaling across the country.

From June through August, warming temperatures and atmospheric moisture combine to produce the hail, tornadoes, and derechos that are now responsible for more cumulative insured losses than tropical cyclones.

Climate change and federal policies are making wildfires more frequent and intense. Migration patterns are increasing the exposure of assets to wildfire threats. And assets that are more vulnerable to wildfires translate into higher costs.