The drivers that make extreme heat so severe were all in play over Independence Day weekend: More people live in areas exposed to extreme heat, existing infrastructure is vulnerable to extreme heat, and cooling is expensive and not universally accessible.

Resilience projects become finance-ready by doing the early work of proving who benefits, quantifying the value of avoided losses, and building the partnerships that make private capital possible.

Three Examples of How Incremental Change Led to Resilience

Early proof points are what eventually unlock scale, and they almost never look like proof when they begin. We need the compounding of resilience over time, and we need to recognize when the next disaster creates a narrow window for rapid investments in resilience—all at once.

By Abby Ross, Contributing Author for The Epicenter and CEO / Founder of The Resiliency Company

Earlier this month, I made the case for incremental change in commercial real estate: the small moves individual stakeholders—from lenders and investors to developers and insurers—can make in the early stages of a project to boost its resilience.

Some readers will look at that article and conclude that the proposed solutions are too small, too slow, not enough. I get it. We urgently need to build for tomorrow’s reality, and sometimes small changes like tweaking an RFP process feel like a drop in the bucket.

In the world of ideas and possibilities, it’s easy to call for a new paradigm of resilient investing across every category of infrastructure in all fifty states. It’s one thing to proclaim, as I have, that we need to make sweeping changes in short order.

It's one thing to call for sweeping changes; it's another to trace the actual path from idea to pilot to policy to national model. Researching that path left me impatient—it can't take this long this time around—but it also clarified something: The early proof points are what eventually unlock scale, and they almost never look like proof when they begin.

Here are three examples of how localized solutions scaled into national models.

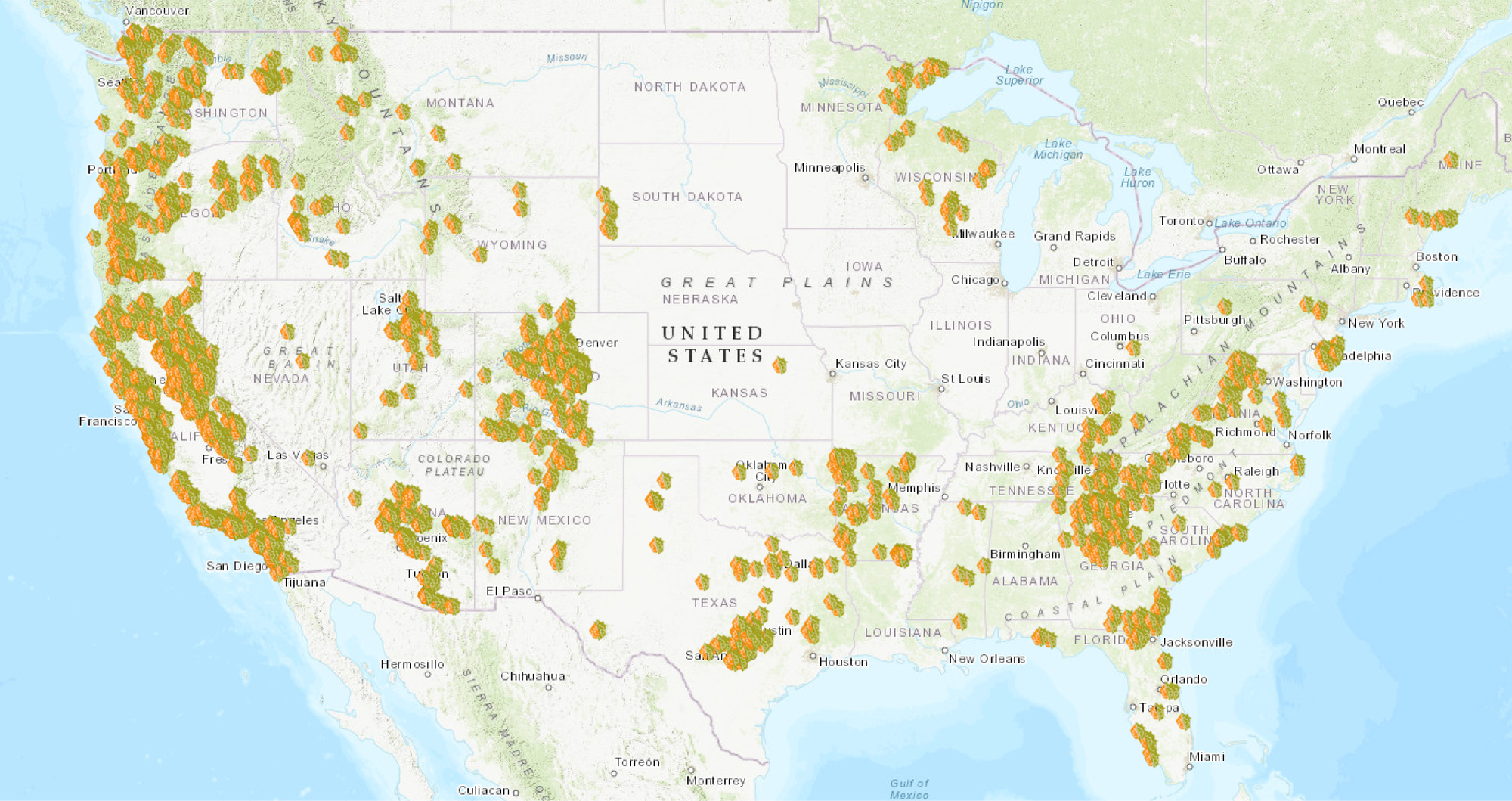

Firewise: Neighborhood-Level Action Is Starting to Matter in California’s Insurance Market

The National Fire Protection Association’s Firewise USA program, which certifies neighborhoods for community-level wildfire resilience activities, recognized its first pilot communities in the early 2000s (it started out as a project in 1986).

For many years, participation remained niche and dependent on motivated local organizers. But interest began to grow, particularly in California, as worsening wildfire exposure and insurance market instability increased pressure for measurable community-level risk reduction.

In 2022, California adopted its “Safer from Wildfires” regulation, which required insurers to incorporate mitigation efforts into underwriting and pricing decisions. Firewise does not guarantee insurability or substantial premium reductions, but the program has grown nationwide (see map below), with nearly 3,000 Firewise sites.

Marin County in California serves as a paragon of the “overnight success” of the Firewise community. Its example shows how incremental policy alignment can build local momentum. The county grew from nine active Firewise sites in 2017 to roughly 90 by 2025, propelled by $86 million in cumulative community investment in wildfire risk reduction over that period. Today, nearly one-quarterof Marin County residents live in a Firewise-designated community.

A Firewise community motivates its residents to prioritize awareness and resilience. When compared to non-Firewise communities, those who live in a Firewise community…

Fix 3.5x more defensible space vulnerabilities per parcel.

Resolve 3.8x more high-priority vulnerabilities per parcel.

Firewise was never conceived as a total solution to California’s insurance crisis. Nor was it written into a bill to shift statewide policy. But even as a voluntary, neighborhood-led initiative, it has gone to scale across the United States.

FORTIFIED: In Alabama, Two Decades of Construction Certification Built a National Model

The Insurance Institute for Business & Home Safety's FORTIFIED program certifies homes and buildings that use construction details proven to perform better in high-wind and rain events, such as hurricanes. The FORTIFIED building standard has three tiers:

FORTIFIED Roof focuses on keeping the roof on and water out through sealed roof decks, stronger roof edges, and impact-resistant shingles.

FORTIFIED Silver adds protection for vulnerable openings like garage doors and chimneys.

FORTIFIED Gold goes the furthest, tying the roof, walls, floors, and foundation together to reinforce the areas of a home that conventional construction may leave susceptible to damage.

Alabama turned FORTIFIED, a technical standard, into a policy model after Hurricanes Ivan and Katrina destabilized the state's coastal insurance market.

In 2009, the state required insurers to offer premium discounts or rate reductions for eligible properties built or retrofitted in coastal communities to approved standards, including IBHS standards.

In 2011, Alabama created Strengthen Alabama Homes, a grant program that helps homeowners retrofit to the FORTIFIED Roof standard.

In 2015, the state expanded the discount framework statewide and extended it to commercial properties.

Each step contributed to a working market mechanism: Homeowners could receive help paying for upgrades, insurers had a verified way to measure reduced risk, and there was market pressure for contractors to learn to build to the standard.

Alabama now offers grants of up to $10,000 for eligible FORTIFIED roof retrofits, while many insurers in the state offer discounts of up to 55% off the wind portion of property insurance premiums (depending on the level of protection).

The FORTIFIED standard was put to the test with Hurricane Sally. A 2025 peer-reviewed study by the University of Alabama's Center for Risk and Insurance Research, commissioned by the Alabama Department of Insurance, analyzed more than 40,000 insured properties in coastal Alabama after the 2020 storm. Compared to conventionally built homes, properties built to FORTIFIED standards performed dramatically better:

FORTIFIED Roof homes had 73% fewer claims, 15% lower claim amounts, and 72% lower total losses.

FORTIFIED Gold homes had 76% fewer claims, 24% lower claim amounts, and 67% lower total losses.

If all regular homes in the study area had been upgraded to FORTIFIED standards, researchers estimated homeowners could have saved up to 65% on out-of-pocket damages, and insurers could have saved up to 75% in payouts.

The success of FORTIFIED has helped it move beyond Alabama. More than 90,000 FORTIFIED homes now span 34 states, and IBHS issued more than 20,000 new designations in 2025.

The success of FORTIFIED in Alabama shows that what starts as a narrow intervention in one insurance market can become an emerging national model for building resilience into the economics of property ownership. (It’s worth noting that FORTIFIED still has room to run in terms of adoption across the country.)

Soft-Story Retrofits: In California, a Decade of Local Ordinances Rewrote Seismic Safety

Soft-story buildings are a familiar feature of California's older housing stock: wood-frame apartment buildings with parking, garage doors, or storefronts on the ground floor and housing above (pictured below). Without enough bracing on the first story, the upper floors can collapse downward during an earthquake.

But the policy response to reinforcing soft-story buildings did not begin with a sweeping mandate. For years, it looked more like the early stages of Firewise or FORTIFIED: fragmented local action and assessments, voluntary screening, technical studies at the municipal level, and some public awareness.

In 2005, California passed legislation encouraging cities to address soft-story seismic safety, opening the door to local retrofit standards. In 2012, FEMA and the Applied Technology Council released FEMA P-807, a "just enough" engineering standard designed to reduce collapse risk affordably—incrementalism written into the code itself.

Then the retrofit standards slowly became local mandates. San Francisco adopted its mandatory ordinance in 2013, covering roughly 5,000 buildings housing 180,000 residents. Los Angeles followed in 2015, after Mayor Eric Garcetti's “Resilience by Design” report, led by USGS seismologist Lucy Jones, reframed seismic retrofit as a citywide recovery issue. LA’s ordinance covers as many as 13,500 buildings. Berkeley, Oakland, Burbank, San Jose, Pasadena, Santa Monica, and West Hollywood have followed. San Jose’s soft-story retrofit ordinance will take effect in 2027.

Like Firewise and FORTIFIED, the lesson in the snowballing of soft-story retrofits across California is that local programs become the scaffolding for more permanent or scaled solutions.

The Need to Balance Impatience with Actual Progress

With the benefit of hindsight, we can trace the progression of pilot to scale, of small to large, of voluntary to policy. But looking forward, it’s hard to spot—and quite frankly to have the faith—that one small step can lead to so much more.

I’m a pragmatist. We need the compounding of resilience over time, and we need to recognize when the next disaster creates a narrow window for rapid investments in resilience—all at once. In my research, I found one of those stories, too.

Waiting for the next disaster is bad planning. So is dismissing the small program that hasn't yet scaled. We need to identify and scale what’s already working. That requires recognizing the early proof points before they look like proof, funding the local programs that haven't yet been replicated, and tying technical standards to dollars so new markets can be created.

Have thoughts to share on this piece, or want to add your voice to the conversation? Reach out!

Sign up for The Epicenter

The Epicenter helps decision makers understand climate risks and discover viable resilience solutions.

The drivers that make extreme heat so severe were all in play over Independence Day weekend: More people live in areas exposed to extreme heat, existing infrastructure is vulnerable to extreme heat, and cooling is expensive and not universally accessible.

By adopting green infrastructure in place of some gray infrastructure, Kansas City reduced the total costs of managing its combined sewer system through 2040 by over $2 billion.