Resilience projects become finance-ready by doing the early work of proving who benefits, quantifying the value of avoided losses, and building the partnerships that make private capital possible.

Insurance markets don't become uninsurable overnight. The transition from insurable to uninsurable is the final stage of a sequence that can take years or decades to play out.

Insurance markets don't become uninsurable overnight. But the transition from insurable to uninsurable is the final stage of a sequence that can take years or decades to play out.

The Weekly: Capital Doesn't Fund Resilience Projects Until Someone Proves Who Benefits

Resilience projects become finance-ready by doing the early work of proving who benefits, quantifying the value of avoided losses, and building the partnerships that make private capital possible.

Insights & ideas on resilience straight to your inbox. Were you forwarded this email? → Subscribe here

- Feature: Funding follows proof that prevention creates value. - In the news: Three ways to de-risk investments in climate-resilient agriculture. - From the archive: AI is closing the data gaps that have limited disaster prediction for decades.

Most capital planning starts with a budget and works forward: figure out what's available, then decide what to fund. A recent article in a blog series by CA FWD and Insurance for Good makes the case that resilience finance runs in the opposite direction: “Capital follows motivated beneficiaries and robust data.”

The closest analog is preventative healthcare, where the earlier the intervention, the better. Success is a problem caught and mitigated before it can become a problem: a disease identified and cured before it could become symptomatic, or in the case of Blue Forest’s Yuba Forest Resilience Bond, a wildfire that didn't happen.

A Case Study in Predevelopment: the Yuba Forest Resilience Bond

Shalini Vajjhala and Caroline George from PRE Collective, who authored the CA FWD article, propose a predevelopment process that asks projects to think through who would lose money if nothing changes, and to use data and modeling to make the clearest possible case that the intervention has financial value.

This is the approach Blue Forest Conservation, a nonprofit conservation finance organization, applied with the Yuba River project, a collaboration of nine organizations focused on protecting 275,000 forested acres in the North Yuba River watershed in Northern California.

The Forest Resilience Bond secures upfront capital from private and philanthropic investors for forest restoration. Then, beneficiaries like utilities and public agencies reimburse investors. The project is preventative: using forest restoration to reduce fire risk and address the negative impacts fire has on water use, water quality, and flood risk. Because the primary dividend is an avoided catastrophe, the model hinges on rigorously quantifying the economic value of a disaster that never happens.

During the predevelopment window, Blue Forest partnered with the World Resources Institute to develop the economic analysis that would make the project’s benefits legible to investors and potential payors like the Yuba Water Agency. They also partnered with academic researchers at UC Merced and Stanford to develop environmental modeling and analysis. On the back of that analysis, they received an early-stage grant from the Rockefeller Foundation’s Zero Gap Portfolio, which specifically sought commercially viable projects.

Then, Blue Forest made its case to potential beneficiaries, like the Yuba Water Agency. Their analysis demonstrated that a healthy watershed protected the water supply and reduced fire and flood risk. With the additional hydropower revenue, the financial value the project would deliver to the Yuba Water Agency exceeded its cost-share contribution.

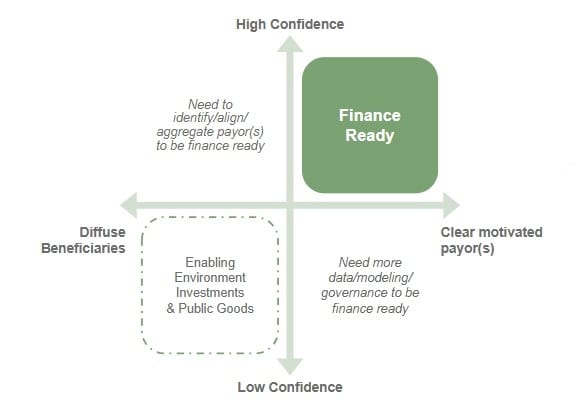

Dimensions of Resilience Funding & Finance

This predevelopment work moved them into the “finance ready” quadrant of the chart above: They had clear data and modeling demonstrating the project’s benefits, and they identified motivated payors who would benefit from the project.

Blue Forest translated ecological outcomes into terms that utilities and investors could act on. The final project included $4 million in upfront investor commitments from four lenders, alongside more than $4.3 million in funding paid by beneficiaries to investors. Private capital enabled the project to be completed six years earlier than it would have under public funding alone. Blue Forest is now developing projects with eight national forests across the West.

Funding follows proof that prevention creates value. Resilience projects become finance-ready by doing the early work of proving who benefits, quantifying the value of avoided losses, and building the partnerships that make private capital possible. Those initial investments in data and collaboration create the conditions for private capital to move.

Making Decisions Under Pressure in Complex Risk Environments | Carrier Management | As climate risks evolve more quickly, insurers are rethinking how they make underwriting decisions without sacrificing rigor. Industry leaders argue that effective decision frameworks, trusted data, AI-assisted analysis, and continuous risk monitoring are becoming important competitive advantages.

California’s Home Insurance Crisis Spreads Beyond Wildfire Country | Stanford Report | A Stanford analysis finds California's insurance crisis is no longer confined to high-risk wildfire communities. As premiums have risen 84% since 2020, and more homebuyers turn to the FAIR Plan, the state’s insurer of last resort, researchers argue that long-term market stability will require both risk-based insurance pricing and greater investment in wildfire mitigation and home hardening.

Tracking Headwaters Management for Wildfire Resilience in California | Public Policy Institute of California | California has set an ambitious goal of treating one million acres of fire-prone landscapes annually to reduce wildfire risk. A new PPIC report finds that treatment efforts are expanding and targeting high-priority areas. It argues that a greater focus on treatment quality and longevity over quantity could improve long-term wildfire resilience.

What Stopped the Sandy Fire? How the Ventura County Fire Department Protected the Simi Valley | Convective Capital | California's Sandy Fire burned 2,000 acres and prompted 10,000 evacuations, yet destroyed just one home, a result of years of resilience investments. Convective Capital’s latest podcast looks at how defensible space and real-time remote sensing technologies helped limit losses.

Read more about resilient public infrastructure and government solutions on The Epicenter here.

Real Estate & Construction

Insurance Costs and Climate Exposure Are Repricing Real Estate Risk | Urban Land Institute | Resilient real estate industry leaders at ULI’s 2026 Resilience Summit described how rising insurance costs, physical risk disclosures, and investor expectations are changing underwriting, asset management, and development decisions. The result: making resilience features increasingly important for protecting long-term property value and cash flow.

The Water Is Rising in Chesapeake Bay. Can Tangier Island Be Saved? | Inside Climate News | As sea levels rise around Virginia’s Tangier Island, engineers and planners are racing to protect homes with seawalls, dredging, marsh restoration, and other resilience projects. It’s another example of the growing role of nature-based construction in extending the lifespan of coastal real estate.

Read more about resilient real estate on The Epicenter here.

Private Investment

The Case for Utility Wildfire Suppression | Latitude Media | As utilities pour billions into wildfire prevention, this article argues the next investment frontier is rapid suppression. It makes the case for utility-funded cameras, drones, aerial resources, and other early-response capabilities that could limit losses when ignitions inevitably occur.

Three Ways to De-Risk Investments in Climate-Resilient Agriculture | PreventionWeb | Climate-resilient farming practices remain underfunded. This article outlines three strategies to unlock private capital and make resilient agriculture more investable: stable policy incentives, climate insurance, and certifications and standards that reward stronger environmental performance.

Read more about private investment on The Epicenter here.

Wildfires: The Drivers Putting People and Assets At Risk | The Epicenter | Climate change and federal policies are making wildfires more frequent and intense. Migration patterns are increasing the exposure of assets to wildfire threats. And assets that are more vulnerable to wildfires translate into higher costs.

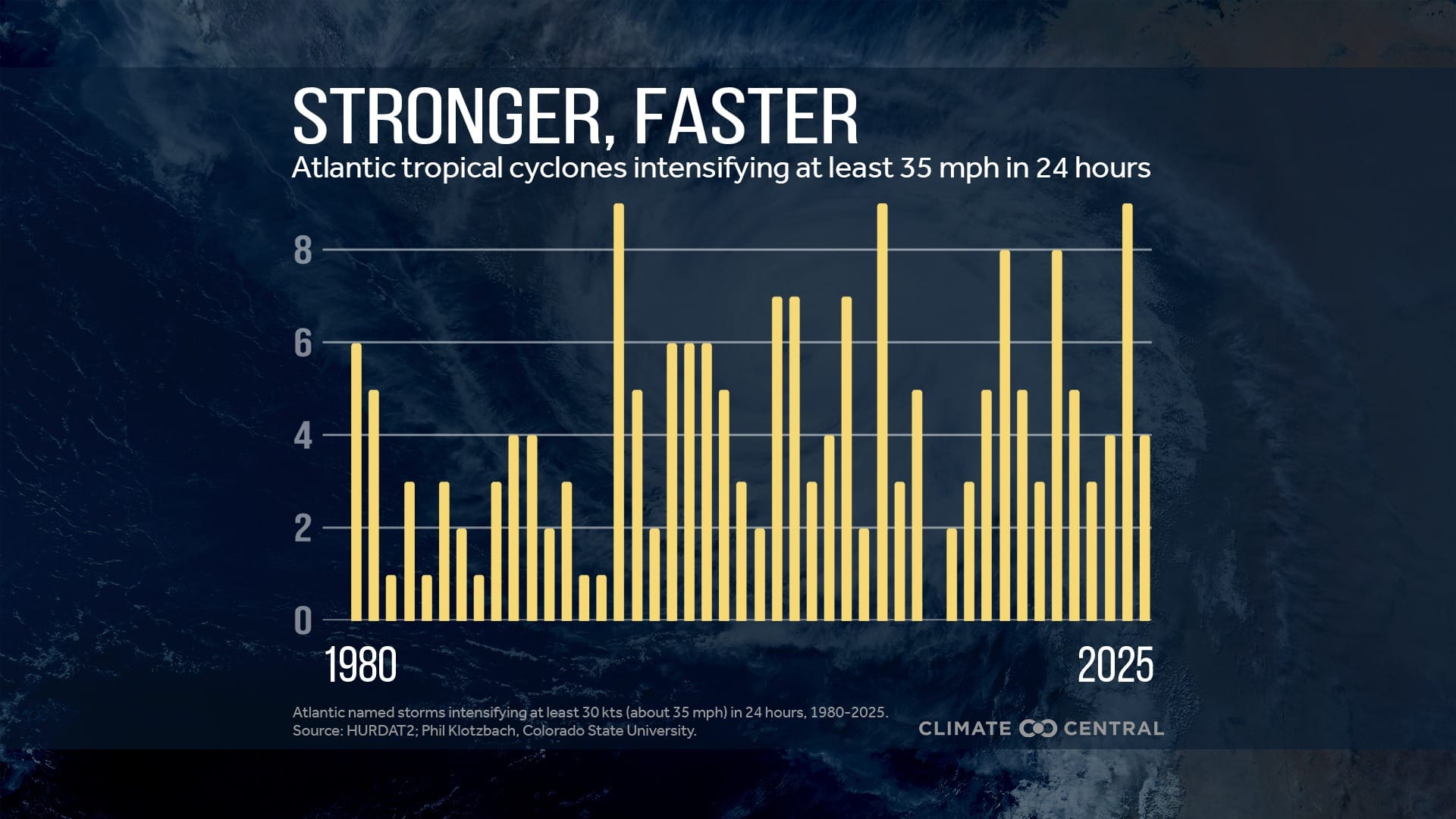

The Chart of the Week

Warmer oceans mean that more tropical cyclones strengthen quickly, a process called rapid intensification.

Have thoughts to share or want to add your voice to the conversation? Reach out!

The Epicenter helps decision makers understand climate risks and discover viable resilience solutions. The Epicenter is an affiliated publication of The Resiliency Company, a 501(c)3 nonprofit dedicated to inspiring and empowering humanity to adapt to the accelerating challenges of the next 100+ years.

Insurance markets don't become uninsurable overnight. The transition from insurable to uninsurable is the final stage of a sequence that can take years or decades to play out.

Insurance markets don't become uninsurable overnight. But the transition from insurable to uninsurable is the final stage of a sequence that can take years or decades to play out.

The economic losses from disasters that are not covered by insurance continue to grow, but resilience projects are generating measurable positive returns.

If today’s funding landscape resembles disconnected wells, then climate resilience requires something closer to a watershed—where resources are intentionally pooled, directed, and circulated across geographies, sectors, and time horizons.